The UK vs. UAE: Is It Time to Consider New Business Horizons?

Recently, the UK narrowly dodged a triple-dip recession. Great news, right? Well, for most people, the reaction is likely a...

Economic Outlook for 2025: What Lies Ahead for the UK Economy

Economic Outlook for 2025: What Lies Ahead for the UK Economy

How Debt is Impacting Retirement Plans: What You Need to Know in 2024

How Debt is Impacting Retirement Plans: What You Need to Know in 2024

The top 10 most expensive UK cities for house prices

The top 10 most expensive UK cities for house prices

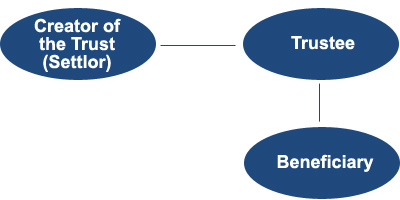

Will an inheritance spoil your children?

Will an inheritance spoil your children?

Rising House Prices in 2024: How Sellers Can Maximize Their Property Value

Rising House Prices in 2024: How Sellers Can Maximize Their Property Value

Recently, the UK narrowly dodged a triple-dip recession. Great news, right? Well, for most people, the reaction is likely a...

Being in debt can be a stressful experience - particularly if you don`t think you`ll be able to repay it...

Taking control of your finances can help you in times of need, and with the cost of living on the...

If you're self-employed in the UK, understanding VAT (Value Added Tax) and when you need to register can be daunting....

Every trader knows that a good platform is essential. Not only does it needs to be fast, safe, and intuitive,...

If you are finding it difficult to make ends meet with your day-to-day financial planning, you might be pleased to...

Life has a way of throwing us curveballs when we least expect it, which might leave us needing financial help....

Protecting the hard-earned money you've accumulated is vital, but if all you're doing is putting it into a standard savings...

Forex trading is one of the most accessible ways to enter the world of investing, offering opportunities for profit from...

Having a history of bad credit can feel like a hindrance to your future financial health, with a low credit...